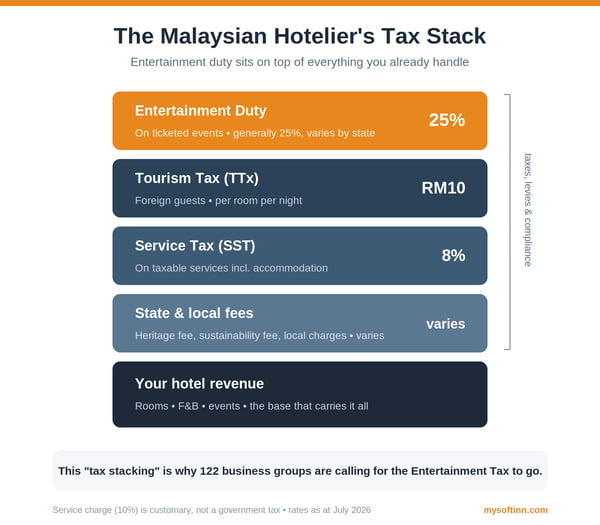

Hotel taxes in Malaysia keep making headlines. On 8 July 2026, the Malaysia Budget & Business Hotel Association (MyBHA) joined a coalition of 122 business groups at a press conference in Petaling Jaya, supporting the industry's call to abolish the Entertainment Tax.

Their argument is simple:

The hospitality industry is already carrying Tourism Tax, SST, local fees, and rising compliance costs;

A tax written in 1953 should not still be on the list.

But here is what we noticed: many hotel owners are not even sure what the Entertainment Tax is, whether it applies to them, or where it sits in their books. So before you form an opinion on the abolition debate, let's get the basics right.

What is the Entertainment Tax?

The Entertainment Tax, officially the Entertainment Duty is a duty imposed on admission to entertainment. It comes from the Entertainments Duty Act 1953 (Act 103), a law enacted during the colonial era when entertainment was considered a luxury.

In practice, it is a percentage charged on ticket or admission prices for entertainment events and venues: concerts, stage performances, cinemas, theme parks, and other ticketed shows. The rate is generally 25% of the admission fee, although actual rates vary by state and by type of event.

Our opinion: A 1953 law taxing "luxury" entertainment makes little sense in 2026, when events and attractions are what fill hotel rooms. On this one, we agree with MyBHA.

Does it apply to all hotels?

No. And this is the most misunderstood part.

The Entertainment Duty is not a tax on room revenue. It does not apply to your nightly rates, your Food & Beverage sales, or your spa treatments. It applies when you charge admission to an entertainment activity.

For a hotel or resort, that typically means:

- Ticketed events on your property: Concerts, dinner shows, New Year countdown parties with paid entry

- Performances by local or international artists where guests buy tickets

- Attraction-style facilities with paid admission (e.g., a resort water park open to the public)

But what about the events that actually fill your banquet hall every weekend?

Weddings, company dinners, seminars?

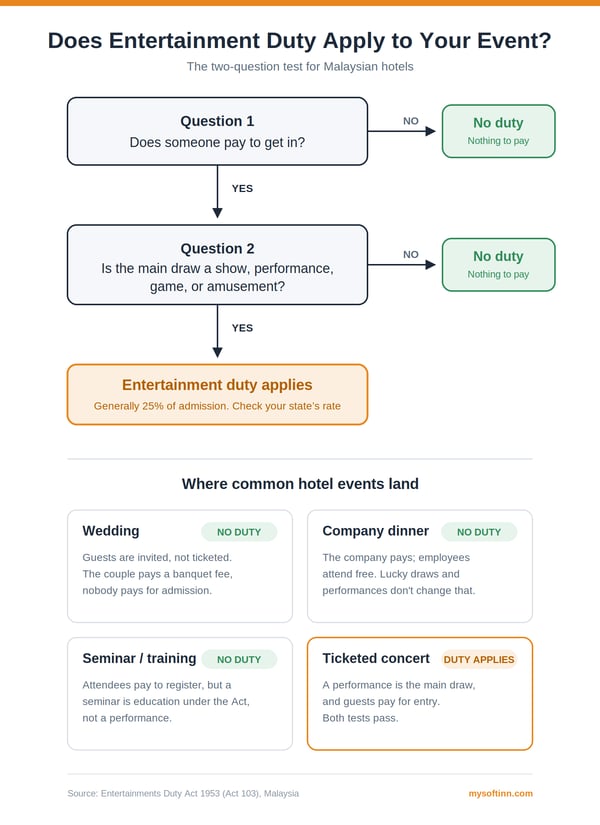

This is where most of the confusion sits. Ask two questions:

(1) Does someone pay to get in?

(2) Is the main draw a show, performance, game, or amusement?

The entertainment duty applies only when the answer to both is yes. The Act defines entertainment as any exhibition, performance, amusement, game, or sport to which persons are admitted for payment, and that "for payment" part is what excludes most hotel events:

- Wedding: Not subject.

The couple pays you a banquet fee; guests are invited, not ticketed. Even with a live band, nobody pays for admission.

- Company annual dinner: Not subject.

The company pays for the banquet; employees attend free. Performances and lucky draws don't change that.

- Seminar, workshop, training: Not subject.

Attendees pay a registration fee, but a seminar is not an entertainment under the Act. It's education, not a performance.

- Ticketed concert, dinner show, countdown party: Subject.

There's a performance, and guests pay for entry. Both tests pass.

One grey area worth knowing:

Charity gala with ticket sales? The duty technically applies. But the Act gives you a way out: inform the Collector at least 14 days before the event and get an exemption certificate. If all the net proceeds go to charity and your event costs stay within 30% of total takings, the duty is refunded. The key point: apply early. The exemption is not automatic.

One more scenario: If your hotel simply rents out a ballroom and the event organiser sells the tickets, the duty obligation generally falls on the event organiser, but if your hotel is the one organising and selling admission, that's you.

So why is MyBHA involved? Because the burden is indirect too.

Higher ticket prices reduce demand for events, concerts, and attractions and fewer events mean fewer room nights. Hotels near event venues feel this even if they never pay a sen of entertainment duty themselves.

When does a hotel have to start paying?

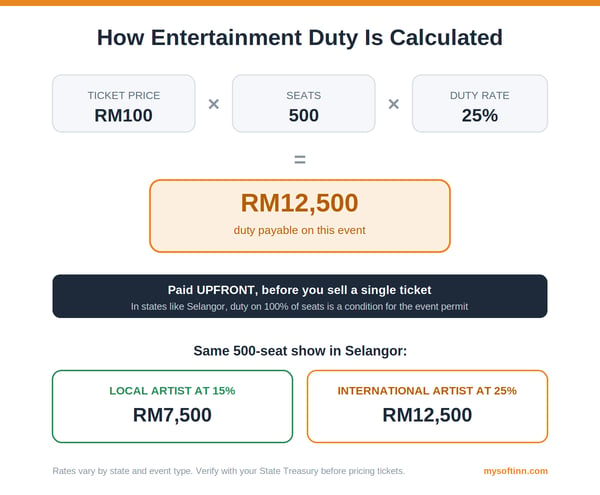

You become liable the moment you charge admission to an entertainment event, and in some states, the duty is payable before the event happens, not after.

Here is the part that catches organisers off guard: in Selangor, for example, the duty must be paid upfront in full, calculated on 100% of seats, before ticket sales begin, it is a condition for the entertainment permit to be issued. You pay the duty on a full house even if you end up selling half the seats.

Timing and exemptions vary by state:

- Federal Territories (KL, Putrajaya, Labuan): Budget 2024 abolished the 25% entertainment duty for local artists' performances in the Federal Territories.

- Selangor: reduced rates from 25% to 15% for local artists and kept 25% for international artists (effective January 2021), and cut theme park duty to as low as 5%. For Visit Selangor Year 2025, the state announced a further reduction of entertainment duties from 25% to 15%.

- Other states set their own rates and exemption policies.

Practical advice: before you plan any ticketed event, check the current rate with your state authority. The rules genuinely differ from state to state, and they keep changing.

How to pay, and to whom?

The Entertainment Duty is state revenue, not federal. Payment goes to the state government, typically through the State Treasury (Perbendaharaan Negeri) via the Collector appointed under the Act. As a reference point, Selangor's entertainment duty rates were gazetted and communicated through letters issued by the Selangor State Treasury.

Entertainment tax (Entertainment Duty) is generally collected from ticket buyers by the venue or event organizer.

In Malacca, a 25% standard entertainment duty usually applies, which must be remitted to your local municipal council. To pay:

- Apply for a Permit: Submit an entertainment permit application to the relevant local authority (e.g., Majlis Bandaraya Melaka Bersejarah or the corresponding district council) prior to the event.

- Calculate the Tax: Calculate the duty based on total ticket admissions. (Note: Rates may vary depending on federal or state exemptions for local artists or specific events).

- Pay Upfront or File: Depending on your council's terms, deposit or pay the estimated tax to secure your event license, or file the remittance at the council office after ticket reconciliation.

- Keep records; some states reconcile actual ticket sales after the event.

Because procedures differ by state, our honest recommendation is: call your state treasury or PBT licensing counter first. It will save you weeks.

How is the tax calculated?

The formula is straightforward:

Entertainment Duty = Duty rate × Admission (ticket) price

Example, using the general 25% rate:

- Ticket price: RM100

- Entertainment duty: RM25 per ticket

- Event with 500 seats: RM100 × 500 × 25% = RM12,500 payable upfront (in states that require payment on full capacity before ticket sales)

In Selangor, the same 500-seat show by a local artist at 15% would be RM7,500; by an international artist at 25%, RM12,500. This is exactly why event organisers say a single foreign act on the bill can push an entire show into the higher bracket, a point raised again at the July 2026 press conference.

Note that this duty sits on top of everything else you already handle: SST on taxable services, Tourism Tax on foreign guests, service charge, and local fees. This tax stacking is the heart of the industry's complaint.

💡 Already doing this math for SST and service charge?

Download the free Hotel Sales Excel Template

Calculates your selling price after tax just enter your price before tax. Entertainment duty follows the same logic.

What happens if you don't pay and why the industry has to pay

The Entertainments Duty Act 1953 has real teeth. Under the Act:

- A proprietor convicted of evading the duty can be fined up to ten times the amount of the unpaid duty.

- The court can cancel the licence granted under laws relating to theatres or places of public amusement, or bar the person from holding such a licence.

- Authorised officers have powers of entry, investigation, and even arrest without warrant in suspected evasion cases.

On top of the legal penalties, non-compliance puts your entertainment permits and by extension your event business, at risk. No permit, no event.

Why does the industry have to pay at all? Because it remains the law, and because entertainment duty is a long-standing source of state government revenue. Selangor alone reported losing more than RM50 million in revenue from a temporary exemption during the pandemic, which tells you how much states collect from this duty. That is also why abolition requires cooperation between Putrajaya and the state governments; the federal government cannot simply switch it off nationwide.

Our take: comply fully today, and support the industry associations pushing for reform. Those are not contradictory positions.

Where does it sit in your P&L?

This is a bookkeeping question we get more often than you'd expect. Here is the practical treatment:

-

If the duty is passed on to the guest (built into the ticket price): It works like other collected taxes (SST, Tourism Tax). The duty portion is not your revenue. Record ticket sales net of the duty, and hold the duty collected as a current liability ("Entertainment Duty Payable") until you remit it to the state. It should never inflate your top line.

-

If the hotel absorbs the duty (you don't raise ticket prices): It becomes a direct operating expense of the event or F&B/banquet department, sitting in departmental expenses, above Gross Operating Profit (GOP). It is not an income tax, so it does not belong below the line with corporate tax.

-

The upfront payment problem: because states like Selangor require payment before ticket sales, the duty first appears as a prepayment (asset) on your balance sheet, then unwinds against ticket sales as the event happens. For smaller hotels running events, this upfront cash outflow is often the real pain more than the tax itself.

If your PMS and accounting integration handles SST and Tourism Tax as separate ledger items, treat entertainment duty the same way: a distinct tax code, never lumped into revenue.

And since you're already in your chart of accounts, this is a good time to get e-invoice ready too.

Download the free Hotel E-Invoice Implementation Guide

Guide to implementing electronic invoicing in Malaysia, ensure compliance and streamlining billing processes.

The takeaway

The Entertainment Tax does not touch most hotels' core room business, but the moment you run ticketed events, it becomes very real: upfront payment, state-by-state rates, and serious penalties for getting it wrong.

Three things to do this week:

- Audit your events calendar. Any ticketed entertainment planned? Check the duty rate in your state before selling a single ticket.

- Set up a proper tax code in your accounting system for entertainment duty, separate from SST and Tourism Tax.

- Watch this space. With 122 business groups, MyBHA, and the Malaysian Tourism Federation now pushing for abolition, the rules may change. We will keep this post updated.

Managing multiple taxes across bookings is exactly the kind of operational complexity a good PMS should absorb for you. If you're still reconciling Tourism Tax, SST, and local fees manually, talk to us , this is what Softinn does.

Read also

Tai Pei Shi

Hi, I am Pei Shi. I am a Technopreneurship student and digital marketing intern in Softinn.

Comments

Recent Posts

Entertainment Tax in Malaysia: What Hoteliers Need to Know

9 Hotel PMS Features for Small Hotel Front Desks in 2026

Low-Cost Hotel Tech for Budget Hotels in 2026

Xiaohongshu (RedNote): How Chinese Travellers Discover Hotels in Malaysia

How to Choose a Hotel Booking Engine in 2026